Introduction

Picture this: you’ve found your dream plot, negotiated a fair price, and you’re just weeks from signing the sale deed, but when a bank suddenly flags an old or unpaid loan which quietly sitting against the very same piece of land. It sounds like a nightmare scenario, but it plays out more often than most buyers realise. Do you believe me when I say, there’s this one document that could have caught this red flag early? Yes. That’s an Encumbrance Certificate.

If you’re navigating a property purchase, sale, or loan application in India, understanding this certificate isn’t optional homework, but it’s a safeguard against inheriting someone else’s financial baggage. So, an Encumbrance Certificate (EC) is an essential legal document verifying that a property is free from financial or legal burdens. It safeguards the interests of the buyers. This blog details the insights about understanding the EC is important to avoid hassle, whether buying, selling, or taking out a loan.

What Exactly Is an Encumbrance Certificate?

In legal terms, an “encumbrance” is any legal claims such as charge or liability attached to a property that isn’t held by the owner, like unpaid loans, mortgages, or pending litigation. An Encumbrance Certificate (EC) is the official record maintained by the Sub-Registrar’s Office that tracks every registered transaction tied to a specific property over a chosen time frame.

In simple words, it answers one crucial question before you commit your money: “Does this property carry any hidden financial or legal strings attached?”. So, now you know, an encumbrance certificate is an important document that contains records of registered transactions about a property. This certificate confirms to the buyers if a land is free from financial or legal liability,

This certificate becomes indispensable in the following key situations:

- Buying or selling immovable property

- Applying for a home loan or a loan against property

- Withdrawing funds from a Provident Fund account to purchase property

- Registering ownership transfer (mutation) after a purchase

- Updating stalled property tax records with local authorities

EC serves as a useful title-check document before a transaction is completed. Buyers can get an encumbrance certificate by visiting the sub-registrar’s office. However, some states, such as Tamil Nadu, Karnataka, Kerala, Telangana and Andhra Pradesh provide an encumbrance certificate online.

The Legal Shield: Why EC Matters

For a buyer, the EC offers a basic but essential layer of due diligence. It helps identify whether the property has been mortgaged to a bank, attached by a court, or transferred earlier. For lenders, the certificate is often mandatory before approving a home loan or using the property as security. Think of it as a “background check” in real estate.

In legal practice, the EC is rarely viewed in isolation. It is usually read along with the title deed, sale deed chain, tax receipts, and municipal or revenue records. This combined review gives a more reliable picture of ownership and encumbrance history.

The Two Faces of an EC

Not all encumbrance certificates look alike, yet the outcome depends entirely on what the records reveal.

| Certificate Showing Transaction History | “Nil” or Clean Certificate |

| Lists every registered sale, mortgage, gift deed, or legal claim recorded against the property in the searched period, including fully repaid loans and settled claims. | Confirms that no registered transactions were found for the period searched — the outcome most buyers hope for. |

It’s worth remembering that a clean certificate only reflects registered dealings. Verbal agreements, unregistered power-of-attorney transfers, or informal family settlements won’t show up, which is why pairing the EC with a review of title deeds and mutation records remains good practice.

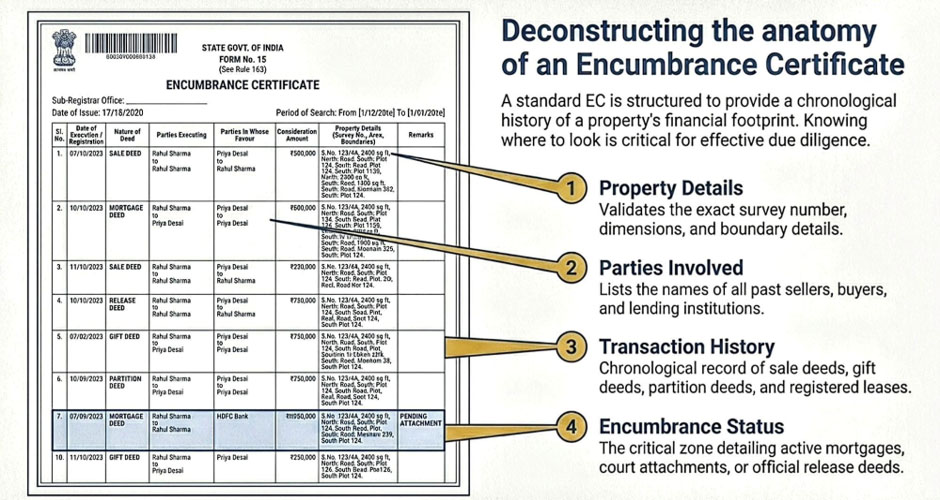

Form 15 vs. Form 16:

Depending on what the records show, you will receive one of two forms:

- Form 15: Issued when the property has a history of registered transactions (sales, loans, or leases) during the search period.

- Form 16 (Nil EC): A “clean chit” certifying that no registered encumbrances were found for the requested timeframe.

The Roadmap: How to Obtain Your EC

You have two routes, depending on your state and patience for paperwork.

The In-Person Route:

- Head to the Sub-Registrar’s Office where the property was originally registered.

- Pick up the application form from the counter.

- Fill it in and attach identity proof, address proof, and the property’s registration documents.

- Submit the form along with the prescribed fee.

- Return after the processing window to collect your certificate.

The Digital Route:

At present, several states including Tamil Nadu, Karnataka, Kerala, Telangana, Andhra Pradesh, and Maharashtra, let you skip the queue entirely through their respective land records portals via online.

- Visit your state’s official property registration website.

- Register for an account (or log in if you already have one).

- Navigate to the online EC application section.

- Select the time period you need searched — for home loans, lenders typically ask for anywhere between 13 and 30 years of records.

- Enter property-specific details such as survey number and document number, and upload supporting files.

- Pay the fee online and submit.

- Track your application status and download the certified copy once it’s ready.

Sample of Encumbrance Certificate

Duration and Validity of the Encumbrance Certificate

Before getting to the application, it’s important to understand the time periods associated with Encumbrance Certificates:

- They can be procured for a maximum period of 30 years.

- The applicant can ask for any period within the 30-year limit; the EC will accordingly display only the transactions registered during that selected period.

- 13 years is the most common duration sought by banks since it’s usually enough to verify the title and spot encumbrances that could affect loan security.

- For property transactions, an EC issued within 30 to 60 days at the time of the transaction is preferable, while banks typically require an EC that’s not older than 3-6 months.

Remember to always request an updated EC when purchasing property or applying for loans to ensure accurate and up-to-date verification. Karnataka’s Kaveri Online Services portal, for instance, has become something of a model for how state governments can digitise land records, allowing applicants to apply, track and download their EC without a single visit to a government office.

The Encumbrance Certificate Karnataka processing time varies based on the application method. For online applications, the processing time is approximately 2-3 working days. In contrast, offline applications may take longer, around 7-15 working days. It may take additional time if any further checks are required from the authorities.

How to Check your Encumbrance Certificate Status

Most state portals feature dedicated sections where applicants can enter their reference number or receipt number to track the status of their online Encumbrance Certificate. It’s advisable to regularly monitor the application and remain aware of any additional requirements or delays. If the application faces rejection due to incomplete documentation or errors, prompt status checking helps to address issues quickly and resubmit if necessary.

Why This Small Certificate Carries Big Weight

For Buyers: the EC acts as a reassurance policy and a proof that the seller genuinely holds a transferable, unburdened title, and that no outstanding dues will land on the new owner’s doorstep.

For Sellers: a clean certificate speeds up negotiations, builds buyer confidence, and doubles as evidence of rightful ownership when the time comes to transfer title.

For Lenders: it’s a non-negotiable checkpoint and no financial institution will sanction a home loan or mortgage without first confirming the property isn’t already pledged elsewhere.

Limits of EC: What the EC Does Not Tell You

While powerful, an EC has its limits. It only reflects registered transactions. It will generally not show:

- Unrecorded oral agreements or family settlements.

- Unregistered equitable mortgages or leases.

- Pending litigation is not always reflected unless it has been formally registered.

- A Nil EC does not guarantee a dispute-free or perfectly clear title.

- The certificate shows recorded entries for a specific period, not the entire ownership history.

- It should be read as one part of due diligence, not the final word on title.

- Fraud, forged documents, and off-record claims may remain outside its scope.

- Outstanding property taxes, water bills, or utility dues.

Practical Checklist for Lawyers and Buyers

Before relying on an EC, it is wise to verify the following:

- Match the property details with the title deed.

- Check the EC for the full relevant period, ideally a longer historical span.

- Look for mortgages, releases, attachments, or prior transfers.

- Confirm whether the certificate shows any nil or active encumbrance.

- Cross-check the EC with tax records, possession details, and other title documents.Investigate any mismatch immediately before closing the transaction.

The Final Word

An Encumbrance Certificate won’t make headlines, but it quietly does more to protect a property transaction than almost any other document in the file. It is not a substitute for full title investigation, but it is a crucial starting point. It helps reduce risk, supports informed decision-making, and adds confidence to property transactions. For anyone buying, financing, or advising on real estate, obtaining and reading the EC carefully should be a standard step in due diligence.

Whether you’re a first-time buyer or seasoned investor, proper Encumbrance Certificate verification protects your interests in today’s complex real estate landscape. Pair it with a lawyer’s review of the title chain, and you’ll walk into your property deal with far fewer surprises waiting on the other side.

Need help verifying a property title or interpreting an Encumbrance Certificate? Meti Legal & Advisory can guide you through the due diligence process with clear, practical legal support. Contact us today to protect your transaction before you sign.

FAQs

An encumbrance certificate is a record showing registered transactions over a property.

For the first time users go to the Kaveri 2.0 portal and click on the register button, enter all the citizen details.

While the Encumbrance Certificate (EC) is not direct proof of ownership, it is a crucial document that helps verify property-related transactions and the property’s legal status.

The timeline for obtaining an Encumbrance Certificate typically varies between 15–20 days. This applies to the offline application process, where you submit your request in person at the Sub Registrar’s office. The duration may vary depending on the state and the office’s workload.

Rufus is a Legal Content Writer at Meti Legal and Advisory and a law student with a keen interest in legal research, public policy, constitutional law, human rights, and corporate law. Passionate about simplifying complex legal concepts, she enjoys researching contemporary legal issues and creating well-researched, accessible content that promotes legal awareness and encourages informed public engagement.